Senior Economist

UCLA Anderson Forecast

UCLA Anderson Forecast

Economic Update:

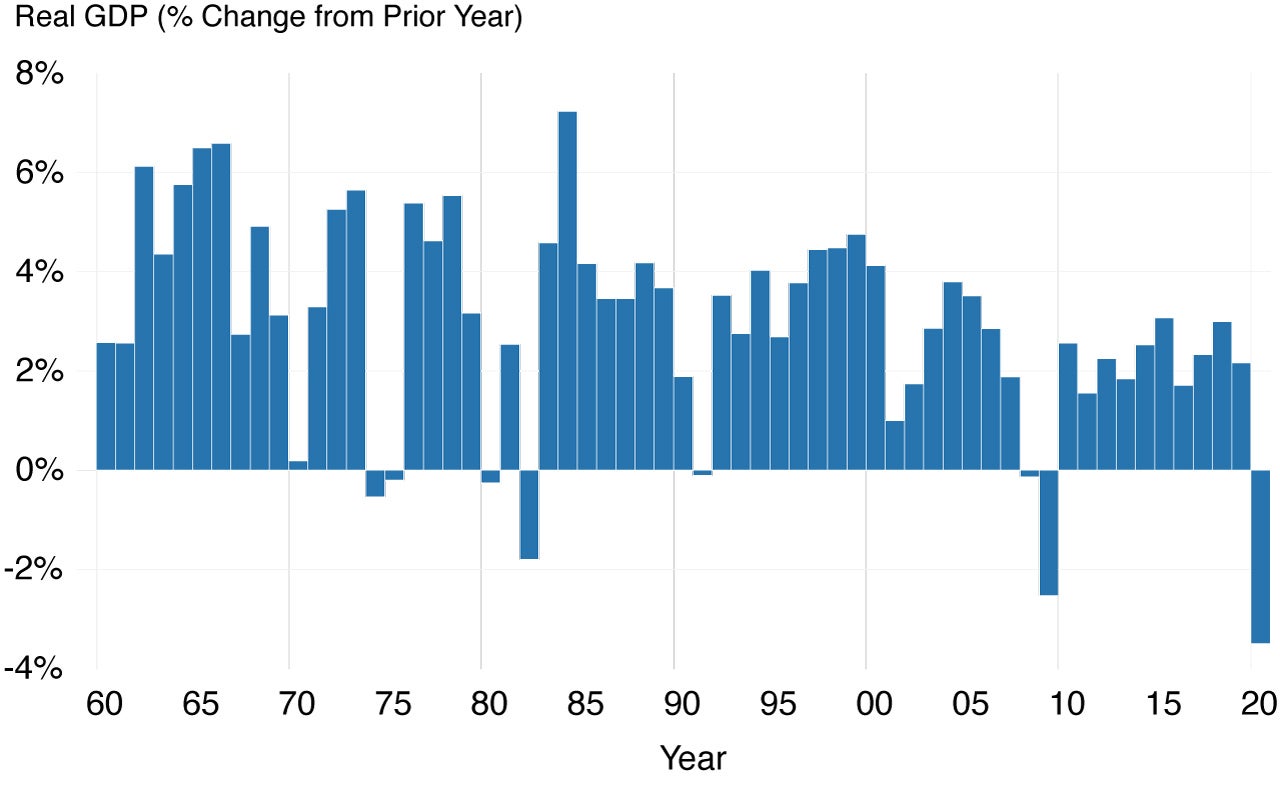

Figure 1. Real GDP declined 3.5% in 2020, the largest annual decline in over 60 years

Source: St. Louis FRED and U.S. Bureau of Economic Analysis

For this edition of Forecast Direct, we talk with Professor Robert Gordon, from Northwestern University, about his book “Rise and Fall of American Growth” and what he sees as the likelihood for faster productivity and economic growth in the coming decades. Be sure to read to the end, where Professor Gordon talks about the best ways to ensure faster growth going forward, through more early-childhood education, more immigration, and affirmative action policies to level the playing field so our society can benefit from the full potential of all individuals. Following is an edited summary of our conversation.

Leo Feler (LF): In your book, “The Rise and Fall of American Growth,” you talk about the great innovations that led to faster economic growth during the last century. Can you walk us through what those were, and why they led to faster growth?

Robert Gordon (RG): Two of them happened within weeks of each other. In 1879, Thomas Edison invented the electric light. Within three years, the first electric power station was operating in Manhattan. Electricity revolutionized everything. It took time. In addition to light, we had machinery in manufacturing and services, the invention of electric refrigeration, and a whole range of home appliances. It took about 40 years from 1880 to 1920 for the effects of electricity to begin to be felt. And then a complete transformation occurred. Rocketing productivity growth in manufacturing in the 1920s, the invention of kitchen appliances which took until the 1950s to become really common. The other invention in 1879 was the first efficient internal combustion engine, which took about 20 years to perfect into the first automobiles. In 1900, there were only 4,000 motor vehicles in the United States, but by 1929, there were 26 million. This was a period of enormous change, getting rid of horses and replacing them with motor vehicles that could go much faster and carry heavier loads. Other inventions of the late 19th century: the telegraph, the telephone, chemicals, plastics, and a complete alteration in the way businesses operated, what they produced, how they produced, and how people lived. Along with all the inventions in the private sector, you had a burst of spending on infrastructure, in particular urban water and sewer infrastructure. In 1870, most people relied on outhouses; by 1929, the majority of urban Americans had indoor bathrooms. As a result of these inventions, we had an unprecedented period of rapid productivity growth. Between 1920 and 1970, the average rate of productivity growth in the United States economy was 3% per year for 50 years. Compare that to the productivity growth rate from 1970 until now, it’s about 1.4%, and for the last decade, it’s only been about 0.6 to 0.7%. This is an enormous slowing down after an extremely fruitful period.

LF: Do you think the innovations of this era – computers, smartphones, medical technology – are likely to affect growth going forward the way the innovations you just mentioned affected growth in the previous century?

RG: Let’s divide the computer age into two parts. One is the part that developed during the 1970s and 80s and came to fruition in the 1990s, with the personal computer, with faster mainframe computers, with the invention of the internet, and the transition of every office and every business from typewriters and paper to flat screens and the internet, with everything stored in computer memory rather than filing cabinets. That first part of the computer revolution brought with it the revival of productivity growth from the slow pace of the 70s and 80s to a relatively rapid 2.5% to 3% per year during 1995 to 2005. But unlike the earlier industrial revolution where 3% productivity growth lasted for 50 years, this time it only lasted for ten years. Most businesses now are doing their day-to-day operations with flat screens and information stored in the cloud, not all that different from how they did things in 2005. In the last 15 years, we’ve had the invention of smartphones and social networks, and what they’ve done is bring enormous amounts of consumer surplus to everyday people of the world. This is not really counted in productivity, it hasn’t changed the way businesses conduct their day-to-day affairs all that much, but what they have done is change the lives of citizens in a way that is not counted in GDP or productivity. It’s possible the amount of consumer welfare we’re getting relative to GDP may be growing at an unprecedented rate.

LF: What do you think are the main headwinds to growth that we face today?

RG: There are many. One of the first is that growth in the 50 years between 1920 and 1970 was supported by the spread of education. At the turn of the 20th century, only about 10% of people had completed high school. That reached 85% by 1970. Progress in extending high school education was over 50 years ago. We’ve had the gradual improvement in the percent of people who go to college, but that’s at a very slow pace, and it has peaked out at about 30% for 4-year colleges and 40% for all post-secondary education. A big problem is that 40% of college graduates, when they leave their 4-year college, cannot find a job that requires a college education. Another headwind includes the reduction in immigration that has occurred in the last 5 years. Much of our innovation comes from people born in foreign countries or the offspring of people born in foreign countries. Many of the top firms in information technology were founded by immigrants. A headwind that seems less important now is rising fiscal debt. We’ve got lots of debt, but little trouble paying for it because interest rates are so low, and in turn, interest rates are low because productivity growth is low.

LF: This pandemic has accelerated technological adoption. We’ve seen companies shift to using Zoom. We’ve seen remote working be fairly successful. We’ve seen the rise of remote teaching and learning. We’ve seen tele-health. You’ve talked in your book about how urbanization and agglomeration increased productivity. Do you see a role for remote working, remote learning, and remote health to do the same now?

RG: This shift to remote working has got to improve productivity because we’re getting the same amount of output without commuting, without office buildings, and without all the goods and services associated with that. We can produce output at home and transmit it to the rest of the economy electronically, whether it’s an insurance claim or medical consultation. We’re producing what people really care about with a lot less input of things like office buildings and transportation. In a profound sense, the movement to working from home is going to make everyone who is capable of working from home more productive. Of course, this leaves out a lot of the rest of the economy. It’s going to create severe costs of adjustments in areas like commercial real estate and transportation. In the short run, there’s going to be a great reduction in productivity in these sectors. I think we’re going to see a period of considerable growth in overall productivity statistics. This has already started in the second and third quarters of 2020. This is because we’ve had a tremendous change in the composition of the labor force. The high-paid people are working from home and are making the same income. It’s the low-paid people who disproportionately account for the loss of employment. In December, U.S. employment was 9.5 million lower than it had been in February of 2020. These lost jobs were disproportionately low-wage. You take the people who are being compensated now and divide that by hours and you get a big jump as the composition has changed away from low-wage workers. This affects not just measured productivity, but also measured average hourly earnings.

LF: There’s optimism that machine learning, artificial intelligence, green technology, investment around infrastructure, the internet of things will fuel higher growth at least through the coming decade. These might not revolutionize our lifestyle the way electrification, indoor plumbing, and combustion engines did in the last century, but do you think they’ll lead to faster productivity growth in the short-run like we saw in the late 90s and early 2000s during the dot com boom?

RG: If we go back to the forecast I made in my book about five years ago, I forecast that over the next 25 years that productivity growth would be 1.2%. It’s only been 0.6% between 2010 and 2019. We have a lot of catching up to do. Looking ahead, just the catching-up from the extraordinarily slow pace of the past decade should give us a sizeable boost. To meet my own forecast of five years ago, productivity growth would have to speed up from the 0.6% I mentioned to 1.5%. That provides a lot of room for innovations that are well underway to make a difference. For instance, electric cars have far fewer moving parts than internal combustion cars. Once we make the transition from internal combustion to electric vehicle manufacture, we’re going to get a $30,000 car made for a lot less input of hours of work. On the issue of artificial intelligence, we tend to exaggerate it as a revolution that’s suddenly around the corner and that will create a night-and-day change in productivity. We’ve had the development of artificial intelligence step-by-step for at least the last 25 years. Everything from voice recognition, voice transcription, automatic language translation, customer service with humans being replaced by voice recognition technology, Amazon examining your orders and telling you what you might be interested in next, legal searches being done by computers, radiology diagnostics being done by computers – all this has been going on for some time. I’m skeptical that there’s a night-and-day revolution in store. All of these things I’ve been mentioning will add up. Of everything we’ve talked about, it’s very possible that the transition to working from home – once we get the rest of the economy sorted out – will give us a sizeable jump in the annual growth of productivity. I would fully expect growth in the decade of the 2020s to be higher than it was in the 2010s, but not as fast as it was between 1995 and 2005. But that was an extraordinary coming together of a lot of technology in a very short amount of time.

LF: From a policy perspective, what could we do as a country to accelerate growth and make it more equal?

RG: I would start at the very beginning, with preschool education. We have an enormous vocabulary gap at age 5, between children whose parents both went to college and live in the home and children who grow up in poverty often with a single parent. I’m all for a massive program of preschool education. If money is scarce, rather than bring education to 3 and 4 year olds to everyone in the middle class, I would spend that money getting it down as low as age 6 months for the poverty population. That would make a tremendous difference. There’s been a lot of economic research on how to bridge the gap of education and upward mobility between those who are lucky enough to have two college-educated parents living at home, who are then very likely to end up in the top 20% of the income distribution, versus those who grow up with a single parent living in poverty, who are likely to end up in the bottom 20% of the income distribution. There are a lot of brains in that bottom 20% who, with a more enlightened system of preschool and elementary education, including charter schools and other ways of singling out low-income children and giving them individual attention, would lead to a much better educated, more productive society. This isn’t immediate. These children need to grow into adults. But if we look out at what our society will be like 20 years from now, this would be the place I would start. I would also open up immigration. I would use the example of Canada, where close to 1% of the population immigrates every year. For us, that would be 3 million people instead of less than 1 million per year. I would introduce an immigration policy similar to that of Canada, Britain, and Australia where you grade potential immigrants with a certain number of points based on their education, language ability, and their skills for employment. We could bring a lot of skilled people in from the rest of the world to bolster our innovation and our productivity. Immigration needs to be loosened up in every direction, from H1B visas, for tech workers, for farm workers – all sorts of reasons for both permanent and temporary immigration. I would encourage a conscious effort to find ways to improve the outcomes for underrepresented minorities in various kinds of high-wage and high-education areas, going out and looking for candidates, subsidizing magnet schools. I’m a big fan of affirmative action. It’s the only way we really have of taking those who are disadvantaged and tilting the playing field a bit in their favor, when we consider all of the advantages of the people who are lucky enough to grow up with college-educated parents.

LF: Thank you, Professor Gordon. I’m hopeful we’ll be able to have, as you mentioned, faster and more equitable growth during these next several decades.