Winter 2021 Survey

Economic Stress and Economic Opportunity

Each economic recession is a little bit different, but this one is a lot different. Through the post-World War II period, recessions have been characterized by downturns in the purchase of goods by households, and by a slackening in housing markets. But today they are not. Consequently, multi-family housing and industrial space remain in the growth portion of their business cycles. But these unusual recession trends are not seen in either retail or office space markets. Both are in a more normal recession pattern of a downward trajectory with the rest of the economy.

Statistical forecast analysis has as its basis the proposition that past statistical relationships hold into the future. A knowledge of those correlations, current data, and perhaps some assumptions about data not yet known, lead to the forecast. Today, the ability to use past data to forecast into the future is more limited than before. However, forward-looking surveys such as the Allen Matkins/UCLA Anderson Forecast California CRE Survey, taken contemporaneously, can enrich our understanding and projections. The Survey has a rich set of questions such that, indirect qualitative inference can be made.

The Allen Matkins/UCLA Anderson Forecast California CRE Survey compiles the views of commercial real estate developers, owners, and investors with respect to markets three years hence. The three-year time horizon was chosen to approximate the average time a new commercial project requires for completion (though projects with significant environmental issues often take much longer). The panelists’ views on vacancy and rental rates are key ingredients to their own business plans for new projects, and as such, the Survey provides insights into new, not yet on the radar, building projects and is a leading indicator of future commercial construction. For example, if a developer were optimistic about economic conditions in Silicon Valley’s office market in 2023, then initial work for a new project with an expected ready-for-occupancy date of 2023 — a business plan, preliminary architecture, and a search for financial backing — would have to begin no later than the latter part of 2020. Although optimism does not always translate into new construction projects, this sentiment is usually a prerequisite for it.

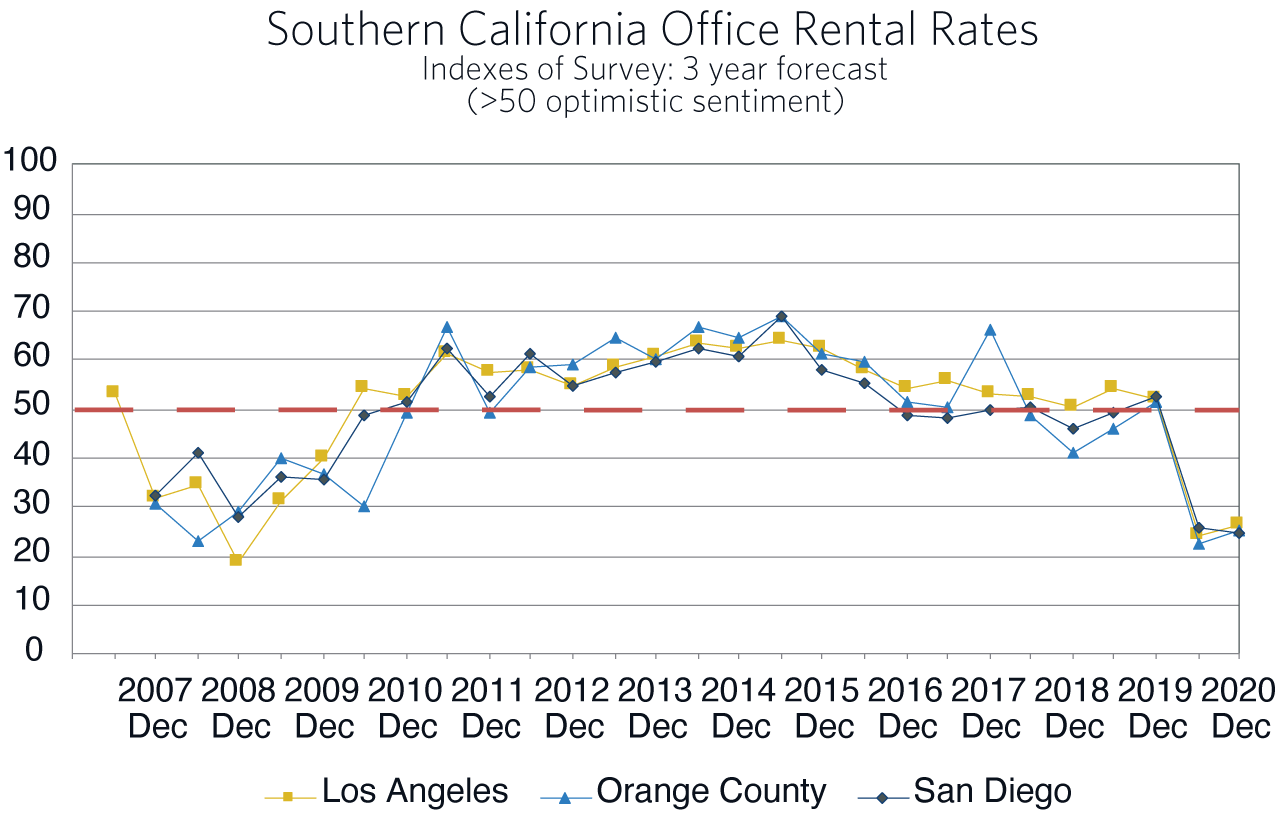

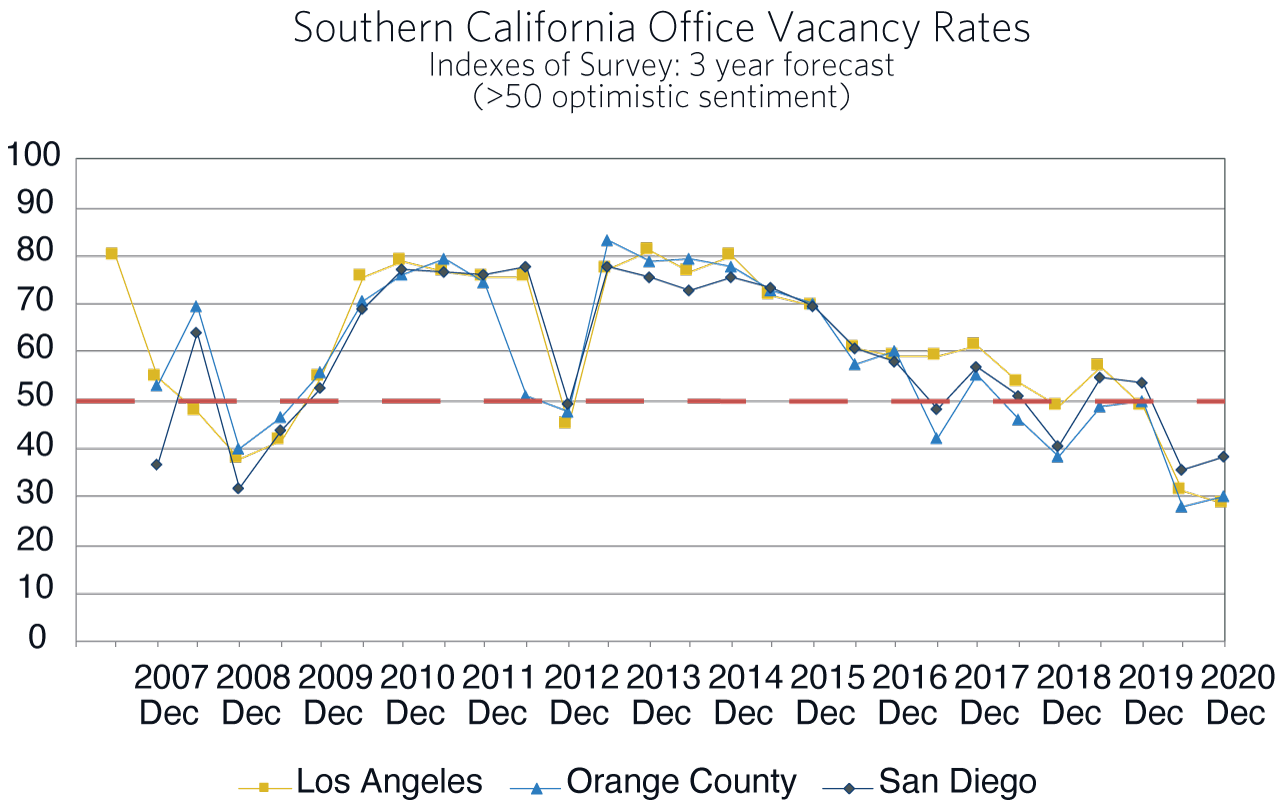

Office Space Markets

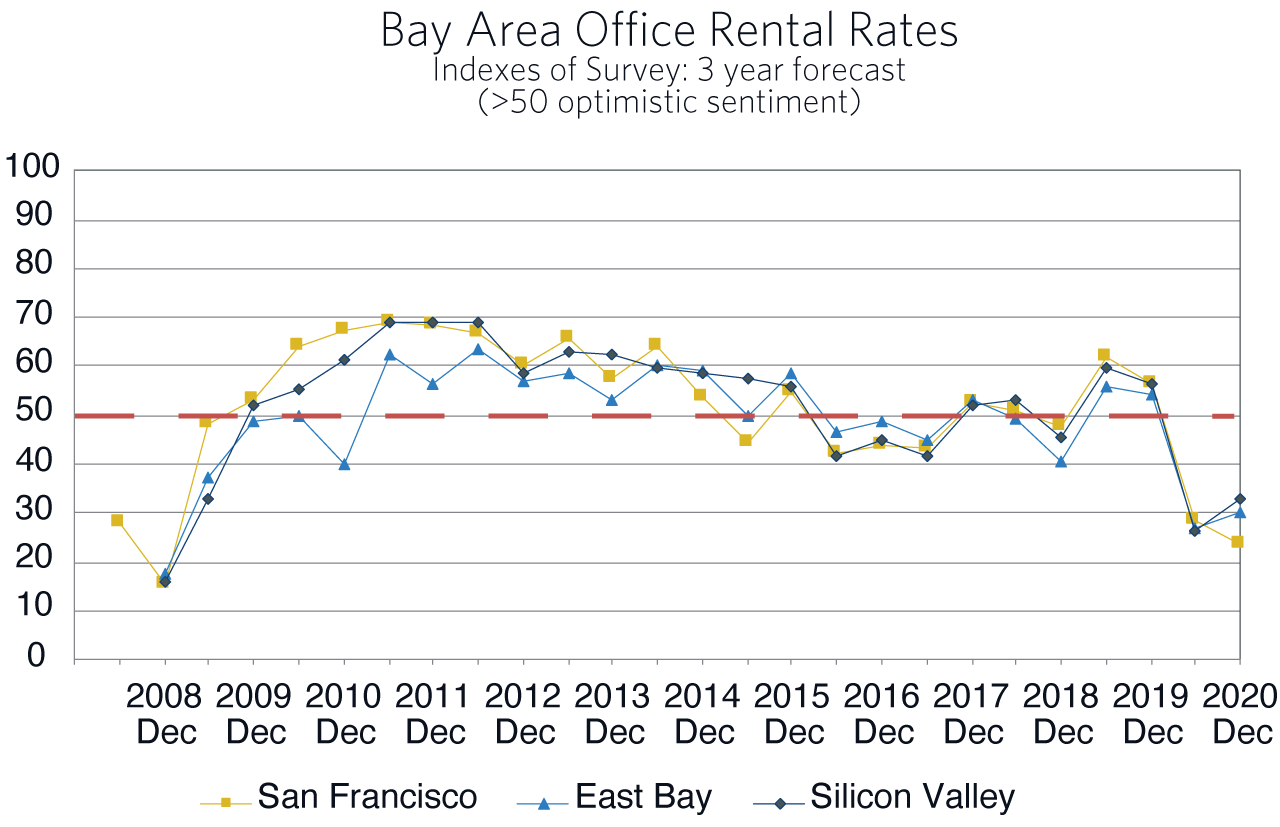

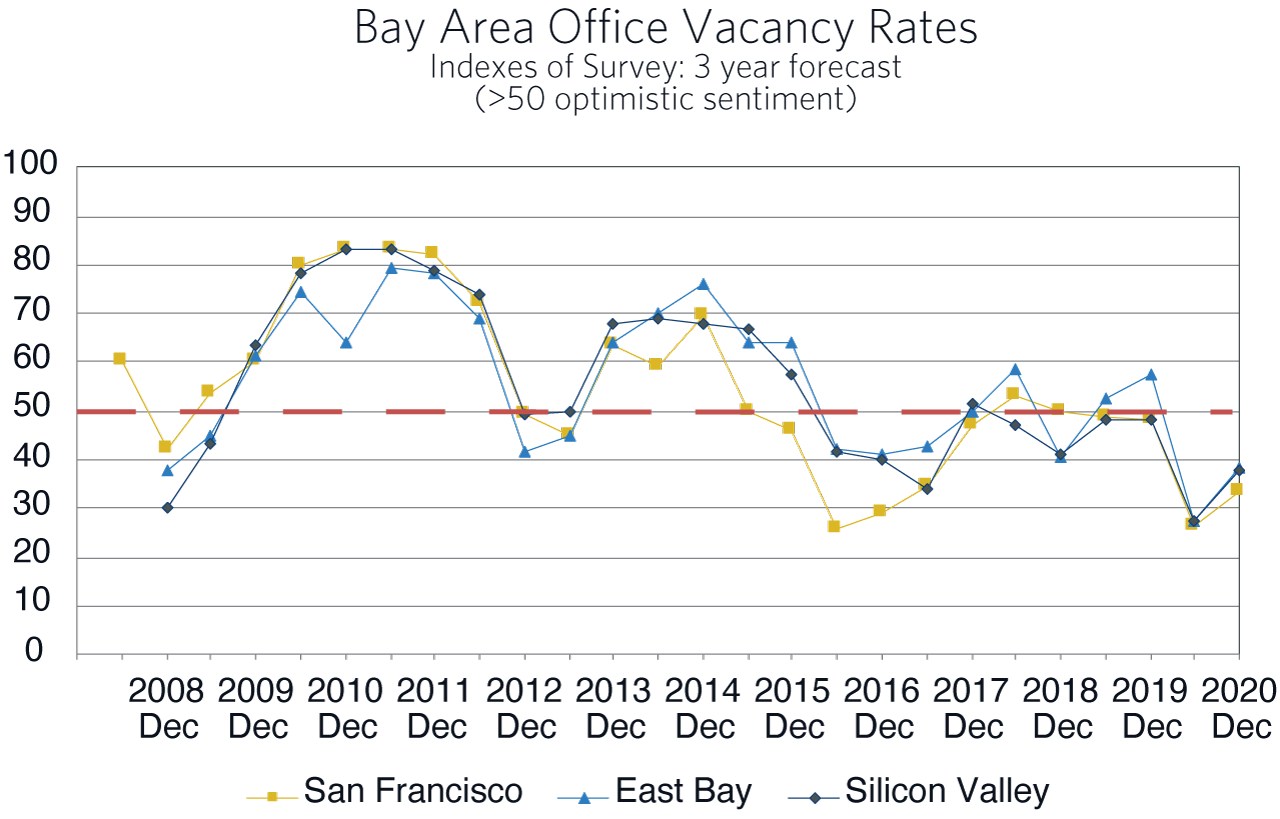

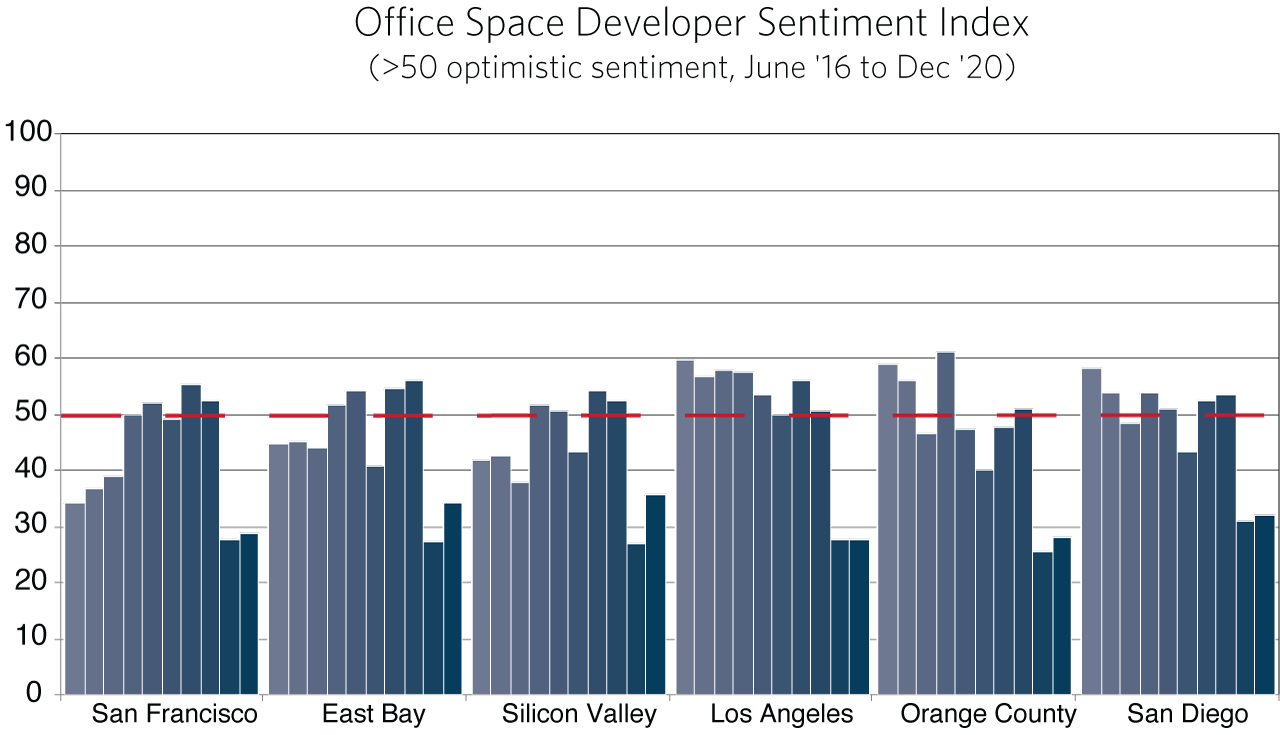

What is the future of the office building? That is the money question on the mind of all who own or develop office space. There will surely be differences, perhaps dramatic ones. Office using employment, as it historically has been defined, will undoubtedly increase in the next expansion as technology intensive industries, health care, education, professional and business services, and information services grow. Health safety and the architecture of the office will be important when the first wave of employees now working remotely return. Will the experience of working from home allow firms to demand less office space? On the surface, the answer is yes. Under the surface, it is not all that clear. The idea of hot-desks, ones with multiple users, has becomes less attractive. Corporate culture, on-the-job training, socially induced creativity, and company socialization suggest no. How does a new hire understand the company and learn from others, and how does a supervisor understand the new hire’s work ethic and innate productivity? The answer is not two hours per day on a meeting web platform. It is only those jobs that, in part or in their entirety, never needed to be in the office in the first place, and that are measured solely by output, that seem to be candidates for complete work-from-home. And, even then, knowing the staff and understanding the goals and requirements might matter. Nevertheless, this remains an open question, particularly with new technologies being developed for improving the productivity of those working from home.

The latest Survey provides a confirmation that the above questions are yet to be settled. While survey participants are confident about the growth in demand for office space between 2020 and 2023, they are pessimistic about the return to investment in new space today. In both Northern and Southern California, the panelists believe that newly built space, in addition to that freed by companies reducing their existing space, will outstrip any near-term increased demand for office space. Compared to last summer’s Survey, our panelists are marginally less pessimistic about 2023, but their sentiment has not turned to optimism. Taking these two surveys together leads to the conclusion that although there will be demand for office reconstruction and for low-rise office building construction, the end of the latest office building boom is at hand.

The headline sentiment remained decidedly negative in the six regions1 we surveyed (Office Space Developer Sentiment Index figure). In Northern California, only 12 percent of our panelists plan to start a new project in the coming year, down from 40 percent who started one or more projects in 2020. In Southern California, there was a similar drop with 17 percent planning on starting a new project compared to 33 percent in 2020. In both regions non-labor building costs were down. However, there was a dramatic rise in sub leases and slow-walking leases from the previous year, and more than half the panelists stated that the pandemic reduced their overall building plans. Across the board there is a wait-and-see sentiment in the office space market, and that portends a downturn in the rate of new development.

The implication of the drop in sentiment is, as in 2008, a continued decrease in new office construction over the ensuing three years. Although half of the Bay Area and Southern California panelists said their plans for the coming 12 months were unaffected by the pandemic, one-third are ramping back development by more than 15 percent from their previous plans. Overall, 75 percent of panelists expressed some stress with current tenant leases. For the one-third that will engage in some new development, the panelists in each market believed that land, building materials, and labor costs would be more favorable. Given the uncertainty about office space demand, these responses seem reasonable and indicate growth in development beginning in late 2021 and a slow return to pre-recession levels.

Retail Markets

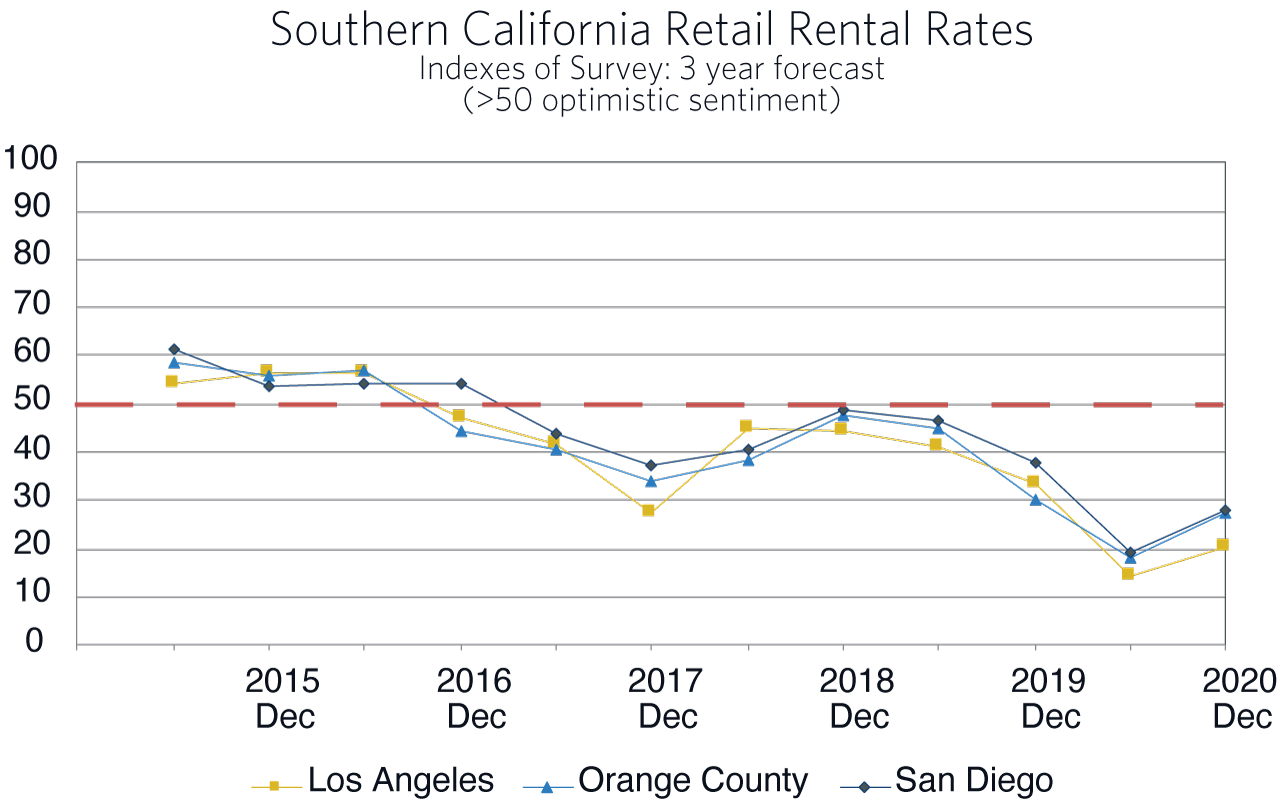

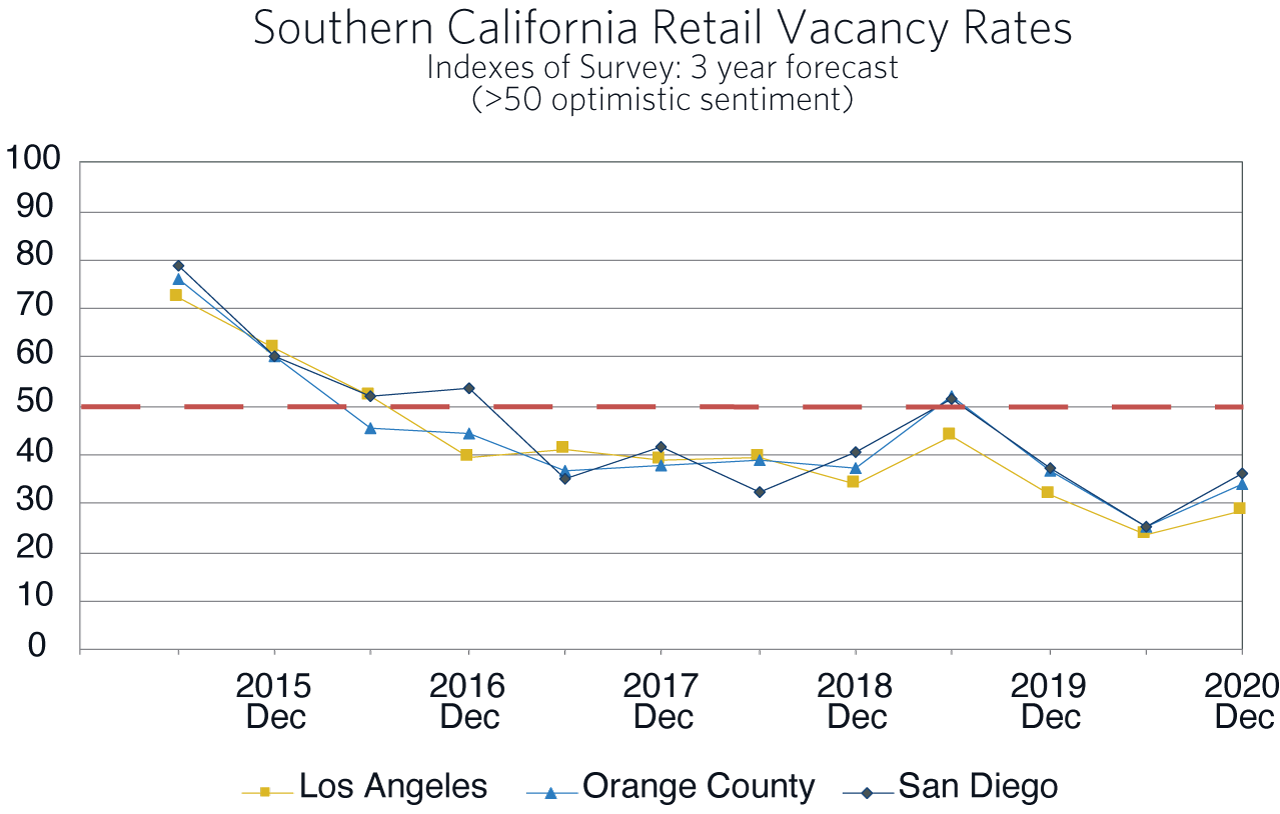

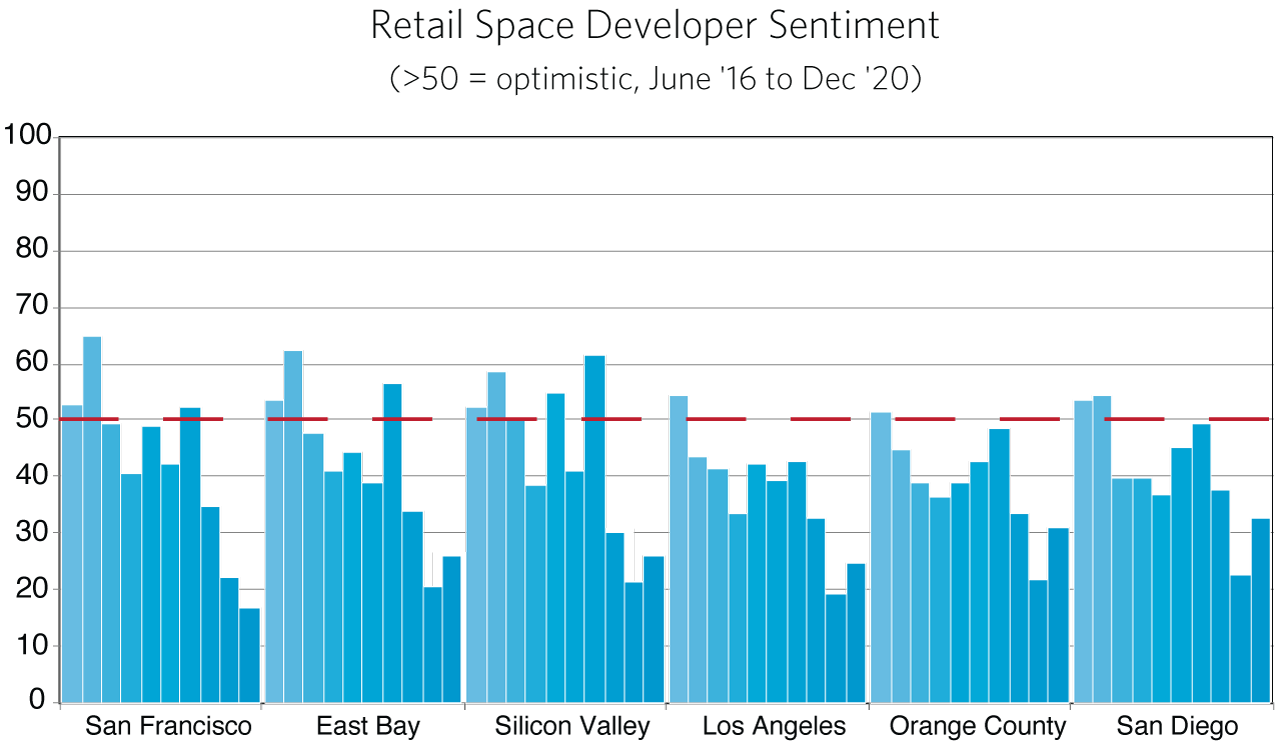

It is said that timing is everything. After the current Allen Matkins/UCLA Anderson Forecast California CRE Survey was completed in early December, the virulent second wave of the pandemic arrived, and that gives us pause in interpreting the results for retail space markets. The improvement in negative sentiment by our panelists throughout the state does not reflect the current closures and reduced in-store capacities of the latest public health measures. As many small retail businesses rely on foot traffic during the holiday season for a successful year, the resurgence of the pandemic will have a further negative impact on retail space.

During the previous economic expansion, retail space struggled. The current recession tripled down on that struggle. First, the loss of household income and the shelter-in-place policies reduced current demand for brick-and-mortar retail. Second, the inability to physically frequent many retail establishments created a new set of online shoppers, and third, increases in the savings rate on the part of households in response to the recession portends less individual consumption. To be sure, some activities will be coming back, particularly personal services and experiential retail. But now, more marginal properties will not find tenants willing to pay sufficient rent to keep the properties in the retail space.

The pessimism expressed in the latest Survey by panelists from both Northern and Southern California is an extension of the trends of the past three years. The current view is that retail properties will be generating significantly lower, if any, returns in 2023 compared to the end of 2020. Fifty-eight percent of the panelists in the Bay Area and sixty-five percent of the panelists in Southern California will not be developing any new properties in the coming 12 months. About the same percentage expect difficulty with current leases and expect reduced property values.

While this is not good news for retail property markets, it does not mean the absence of solid targeted opportunities. New housing developments, whether they are multi-family or single-family, generally require nearby retail. The booming housing market will continue to generate this demand. New Haven Marketplace, being built in Ontario Ranch for the residents of the new Brookfield development is a case in point. But, overall, the level of new retail property construction is expected to significantly decline from 2020 through 2023 and some existing space, lacking sufficient demand, will be converted to other uses.

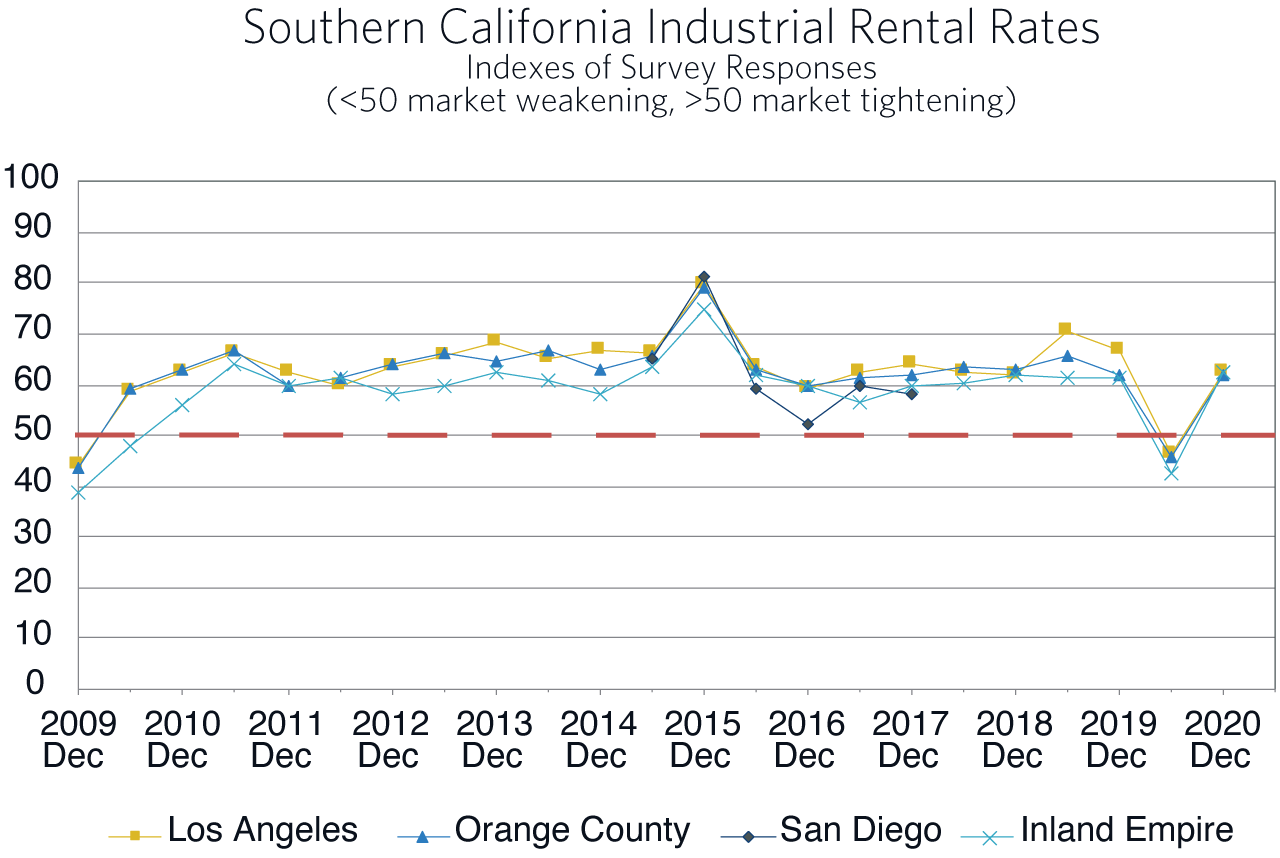

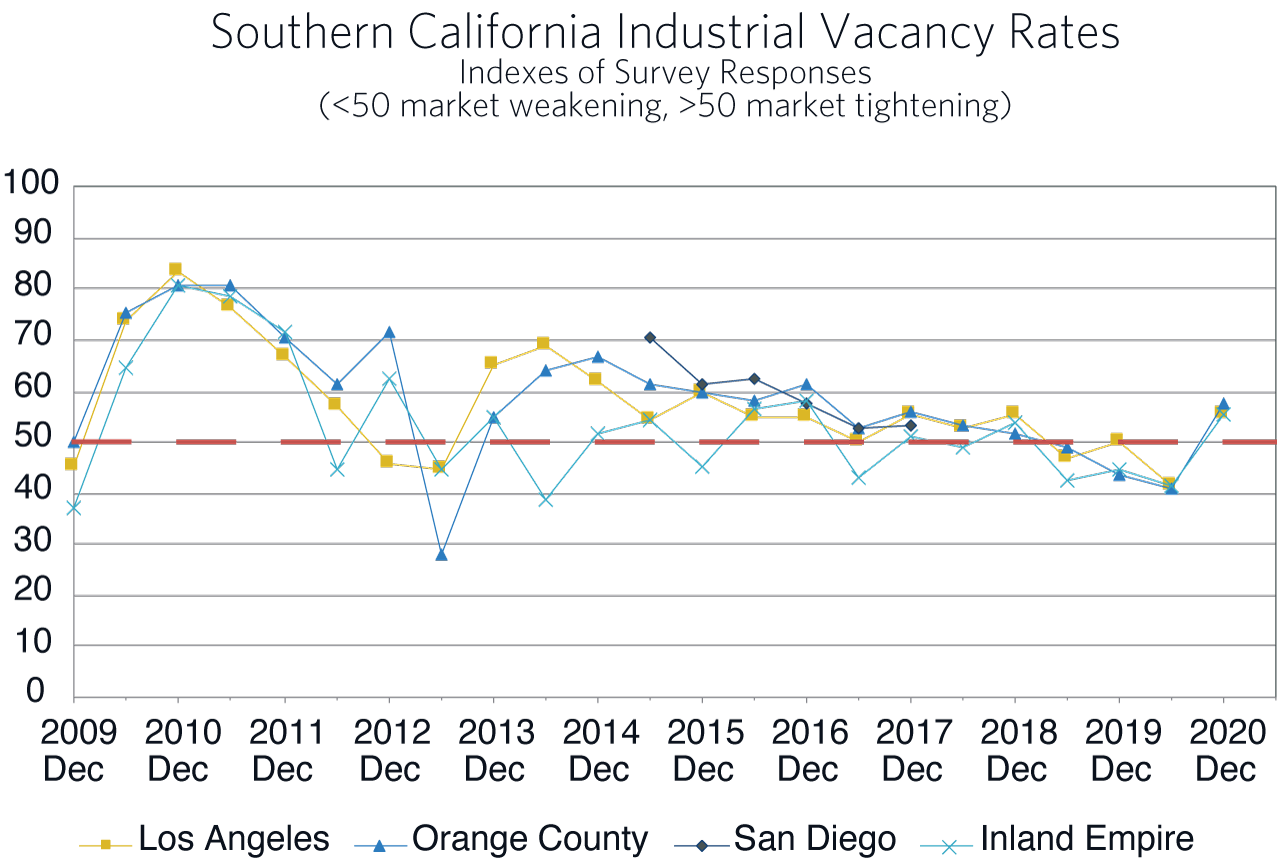

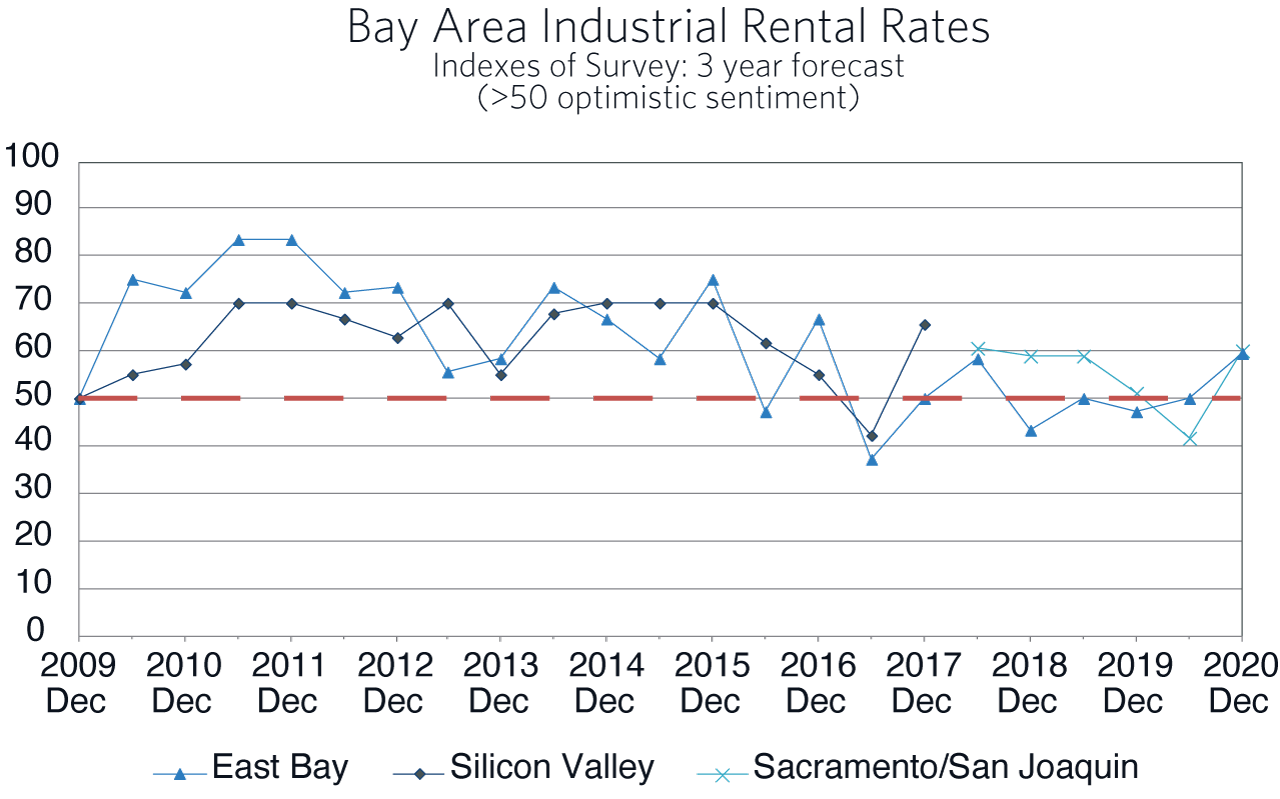

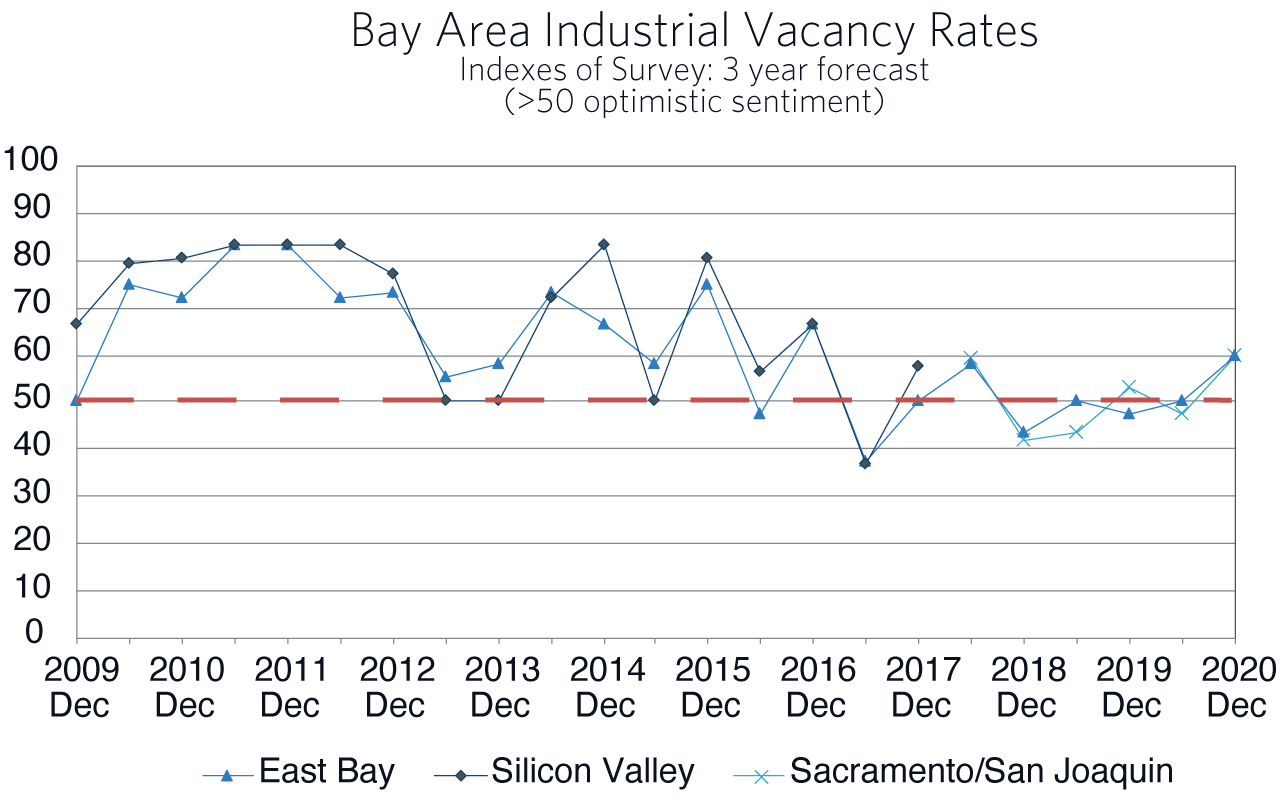

Industrial Space Markets

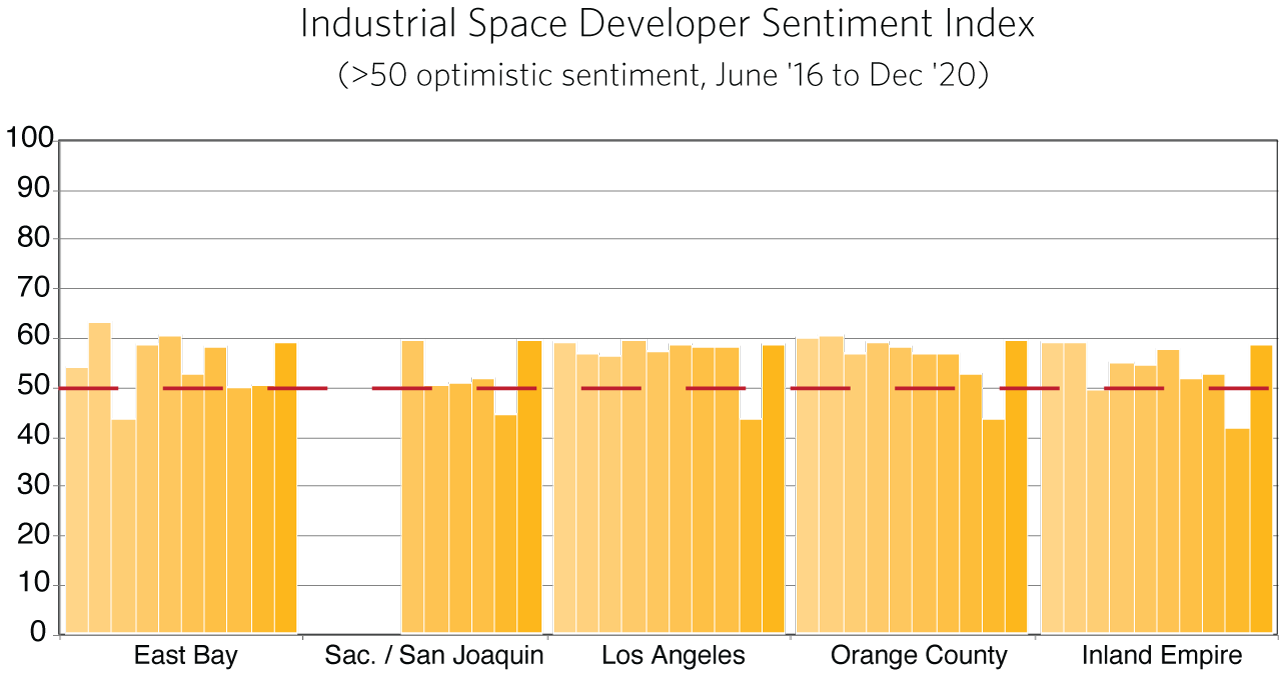

Though the pandemic has dampened the market for office space, the opposite is true for industrial properties. Industrial markets over the past several years have seen consistently high occupancy rates and superior lease rate growth. Sentiment expressed in the June Survey dropped precipitously in all markets (Industrial Space Developer Sentiment Index Figure), and that is logical. We were in a deep recession and pessimism about the coming couple of years was the order of the day. However, vacancy rates remain extremely low. At the end of September, Los Angeles and Inland Empire vacancy rates were under 4 percent, and from Sacramento to the East Bay between 4 percent and 5 percent. As expected, industrial space sentiment has come roaring back, and it is now at levels of optimism about the coming three years that has not been seen for many years.

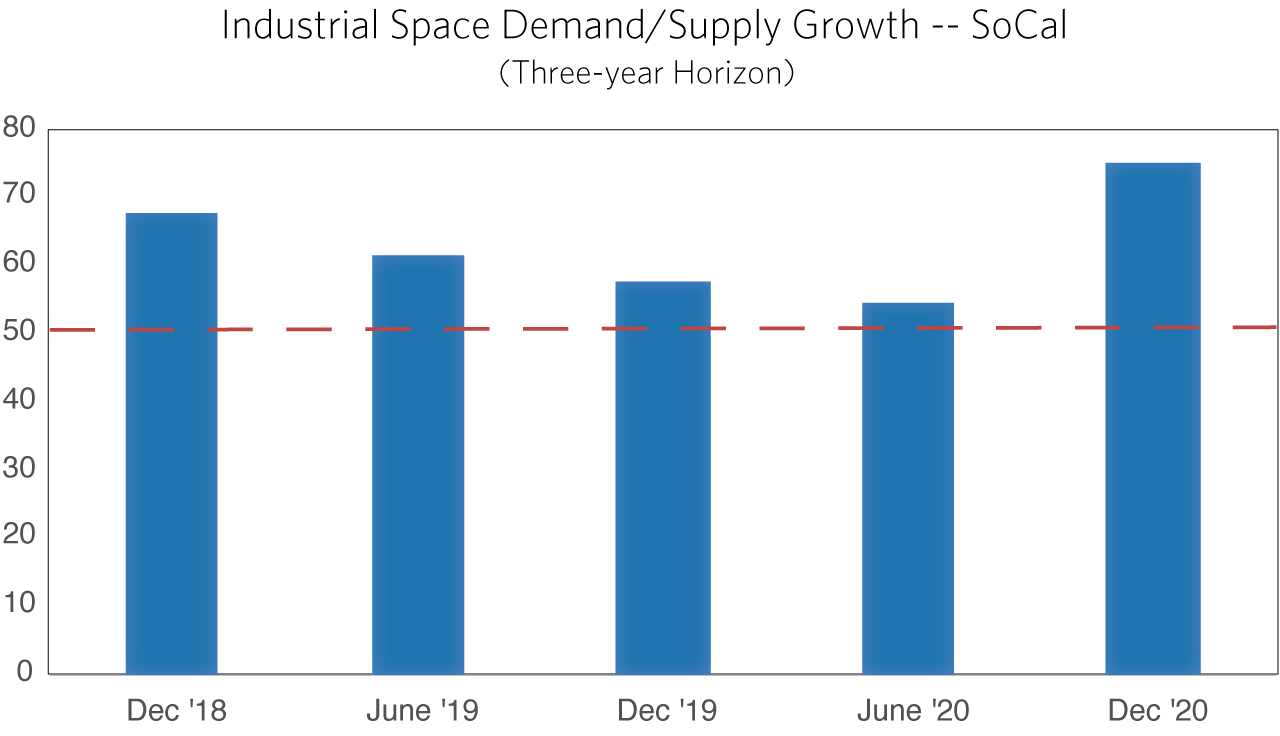

In both Northern and Southern California, the developer sentiment index rebounded to significantly over 50, the dividing line between optimism and pessimism. In each market surveyed, the expectation was for lease rate increases to exceed the rate of inflation and for the already low vacancy rates to be even lower by 2023. Behind this sentiment is a view by the panelists about online shopping induced demand for industrial space, and about the expected increase in the stock of that space. The figure below shows demand and supply question responses for Southern California over the past two and a half years. A value over 50 indicates that the panelists expect the demand for space to increase faster than the supply of available space.

The dramatic change in household buying habits during the pandemic is illustrated by the latest data on retail sales from the US Census Bureau. It reported that overall retail sales in the United States were down 1.1 percent from October to November. However, non-store retail was up by 29 percent. While some of the shift to online purchases will reverse when the pandemic is behind us, the experience of online shopping has most likely changed household purchasing permanently.

Although our panelists are very optimistic about the next three years, their current building plans are only marginally higher than their pre-pandemic plans. In both Northern and Southern California, approximately 30 percent of the panelists stated that the experience of the recession has caused them to consider increasing the amount of development they will undertake. Therefore, our expectation is for a new wave of warehouse building over the coming three years.

Multi-Family Housing Space Markets

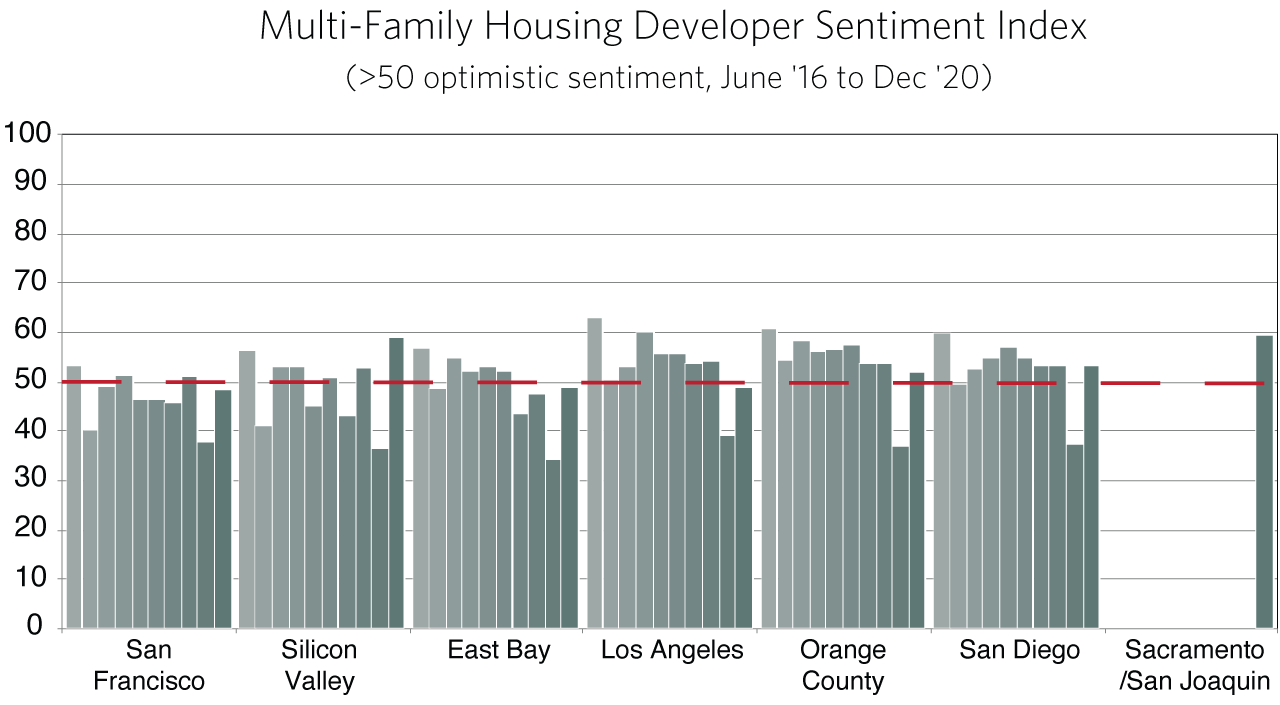

Multi-family developer sentiment is back, at least in Silicon Valley, Orange County, and San Diego. The other four markets surveyed–the East Bay, Sacramento and the Delta, San Francisco, and Los Angeles–saw an improvement in developer sentiment, but our panelists in these markets do not see 2023 as having higher occupancy and rental rates compared to today.

The East Bay and Sacramento regions have significant government employment. Both are also home to bedroom communities for less affluent workers commuting to the less affordable coastal cities for work. In this recession, government employment and sectors with a higher proportion of lower income workers have seen the greatest decline in employment. Sentiment, and consequently development of multi-family housing is expected to improve in these regions as state tax revenues are now exceeding expectations.

For the two other markets where the panelists were pessimistic, there have been dramatic declines in rental rates. In San Francisco they have fallen 20 to 30 percent and in Los Angeles the decline is about seven percent. Some of this weakness is due to students not coming to campus, and some is due to information economy workers now working from home and not needing a pied-à-terre in the city. Some is due to an exodus of households that were contemplating a move to the suburbs to welcome children in a few years, and in the wake of the pandemic and low mortgage interest rates have decided to move earlier. Finally, this recession has had a major impact on low-wage workers. Less affluent households typically have less savings and at least some of these households are likely economizing on housing by doubling up or moving further afield. Though we do not have data on how much of each has occurred, each is likely a factor in the declining coastal city rents.

Though declining rents surely impact the business plans for multi-family developers, they have not had much impact on the actual level of building. The reason is that while rents are down, they are down from very high levels. Even after the dramatic drop in San Francisco, the average rental rate for a studio in November 2020 as reported by Bloomberg was $2,100. With uncertainty as to whether or not rents will rebound in the near term, the pessimism expressed by our panelists in San Francisco and Los Angeles portend fewer near-term developments in these markets.

However, the average percentage of developer/operator panelists who do not have plans to start new projects over the next 12 months, either because they were fully booked with ongoing construction or because they do not see a lucrative opportunity at this time, has fallen to 34 percent from almost half this time last year. Moreover, in Northern California half of the panelists will begin more than one multi-family development in the coming year and in Southern California one-third will. We expect multi-family development to continue to grow in California, though the pandemic has changed the nature of the demand for apartments, both geographically and in their footprint.

As the economy grows, the demand for housing throughout California will grow with it. Though the UCLA Anderson Forecast is looking at an extended post-pandemic recovery of jobs throughout the state, and there remains a great deal of uncertainty with regard to the current public health crisis, the market for multi-family housing remaining robust seems likely.

The Survey in Perspective

Scuba divers know that when navigating to and from the shore, one does not use fish as reference points as they move before you know it. This is a lesson we should take to prognostication during a pandemic-induced recession. There are many moving parts. Several vaccines have been approved for use and are in the process of being distributed. But a second wave of the pandemic is upon us and the rapidity of the adoption of the vaccine, as well as the abatement of the pandemic remain uncertain. When the public health crisis is in the rear-view mirror, then any changes in the trends in commercial real estate will become clearer. For now, if we ignore the fish and look for a path related to the pre-pandemic markets, there are some clear trends.

Is the office market dead? No, not likely, even though many are now working from home. But what it will look like post-pandemic is still uncertain. So, our forecast from the Survey is for a near-term pullback in office construction, with the possibility of a rapid turnaround. Is everyone moving out of the city? Some are, but some will be moving back in and rents will equilibrate. And in a tight housing market, a short-term easing does not have a significant impact on new development. The current Survey confirms a continuation of the aggregate trends previously seen in industrial and multi-family spaces, a more nuanced hiatus in the office space, and a steeper downturn in the retail space. This is a most unusual recession. The implication of our two Surveys since it began is that in general, commercial real estate will have an easier path ahead than in most recessions, though there are a few, possibly large, rocks in the path, particularly for office and retail properties.