Innumerable nudges help savings accumulation; now researchers turn to decumulation

As gnarly as it has been to get workers to save for retirement, behavioral economists are now focused on retirement challenge 2.0: nudging the first 401(k) and IRA savers to become smart retirement spenders.

When DIY retirement investing arrived more than 35 years ago in the form of 401(k)s, 403(b)s and individual retirement accounts (IRAs), it gave the burgeoning field of behavioral economics a fertile petri dish in which to work.

Baby Boomers were just gliding into their prime earning years when it soon became clear (at least to academics and folks running the retirement plans) that left to our foibles, we aren’t exactly hardwired to save and, more important, save enough.

Opt In to the Review Monthly Email Update.

Procrastination, inertia, loss aversion and the pernicious challenge of delayed gratification were just some of the behavioral norms working against retirement planning success.

Long before the notion of behavioral nudges went mainstream, UCLA Anderson’s Shlomo Benartzi and the University of Chicago’s Richard Thaler produced research on how to help workers boost their retirement savings. They found that most workers wouldn’t flinch at having their contribution rates automatically increased when they received a raise, a tactic known as auto-escalation. The Save More Tomorrow™ strategy Benartzi and Thaler laid out in 2004 is now a key lever employers are pulling to help increase retirement preparedness. More than 60 percent of firms surveyed by benefits consultant Callan had an automatic escalation feature in their retirement plan in 2016, a sharp increase from 46 percent a year earlier. And more than half of firms that have yet to get on the auto escalation bandwagon say they are angling to add the feature to their plans in 2017.

Auto Everything

In addition to auto enrollment (opt out versus opt in), auto escalation and auto rebalancing, federal regulations were tweaked to allow plans to enroll new participants by default into target-date mutual funds, which deliver auto-diversification in a mix of stocks and bonds deemed appropriate for a given investment time horizon.

But there has been less systemic focus on how to help retirement savers nearing the end of their careers convert their retirement accounts into a sustainable source of income throughout retirement and find the right rates at which to spend.

The leading edge of the Baby Boomers is the first DIY retirement cohort that must become retirement spending experts, supplanting the pension department at former employers for their parents and grandparents.

And that comes with a high degree of difficulty. After spending years in an accumulation mode where the only message has been save, save and save more, it’s a big ask to suggest retirees deftly make a 180-degree pivot and become masters of decumulation. The complexity of the variables involved in a decumulation strategy — life expectancy, expected portfolio returns, estimating retirement spending needs (especially health care) over a 30-year span, and the impact of inflation — makes three-dimensional chess look like a game of Go Fish by comparison. Nobel Laureate William Sharpe, the godfather of the Capital Asset Pricing Model, described the decumulation challenge as the “nastiest, hardest” problem in finance, in a recent interview with Bloomberg View’s Barry Ritholtz.

Making matters worse is that retirement plan sponsors and government regulators have been slow to bring the nudge mentality that is now widespread on the accumulation side of retirement saving to bear on the decumulation stage. Economists have explained this anomaly as having built retirement airplanes that can take off and fly, but do not have any landing gear in place.

UCLA Anderson’s behavioral scholars are delivering research to help drive the creation of systemic nudges directed at helping retirees navigate the decumulation stage of their DIY retirement odyssey. Benartzi, along with Anderson colleagues Suzanne Shu, Hal Hershfield and Robert Zeithammer, is among a squadron of academics now focused on helping retirement savers make the transition to retirement spenders. At stake is not just financial security — making sure basic needs can be financed throughout retirement — but also giving the conscientious savers of the past few decades the confidence and peace of mind to spend more in retirement without fear of running out of money.

Yes, spend more; though, sadly, this applies to only a small subset of savers.

Researchers at Texas Tech and William Patterson University pored over retiree spending data and opined that, on average, retirees with median wealth could safely afford to increase their spending by 8 percent annually. Households with investable retirement assets north of $650,000 (the highest quintile in the study) had a “retirement consumption gap” of more than 30 percent. That translates to an estimated $27,500 to $49,800 a year that might be spent without endangering long-term security. Over a full retirement, that computes to forgone consumption of $820,000 to nearly $1.5 million. The authors also ran the numbers for households with above-average wealth, assuming that 40 percent of that wealth was cordoned off in reserve. That is, as a safety net. They still found that there was plenty more spending that could occur with the remaining 60 percent. They estimate that under-spending over a 30-year retirement ranged from $272,000 to $1.165 million. (Any voice in the retirement field that suggests under-spending, of course, raises concerns about undermining the still-uncompleted work of getting more people to save enough.)

The authors grant that, while leaving a bequest to the kids, grandkids or charity of choice may be at play, also a factor driving chronic under-spending is the complexity of devising and maintaining a sustainable decumulation plan.

The Live-To, Die-By Gap

Life expectancy is perhaps the most daunting factor retirees must grapple with. As if it’s not tough enough to contemplate one’s mortality, it turns out that we’re also thwarted by how life span (the polite version of mortality) is framed by financial services firms.

UCLA Anderson’s Shu coauthored research with Duke’s John Payne and Namika Sagara, and Columbia’s Kirstin Appelt and Eric Johnson, that compared lifespan expectations based on whether the question was phrased to ask what age you expect to “live to” versus what age you expect to “die by.” The median age for the live-to frame was 85 and for the die-by frame it was 75. “This 10-year difference in the median expected age of being dead or alive is not only statistically significant but also highly meaningful to a number of important life decisions, such as how to finance one’s consumption during retirement,” the authors wrote. That is, if you think you’re going to live longer, you might be attuned to building later-life income streams into a retirement plan by purchasing products such as standard fixed annuities, longevity annuities and long-term care insurance.

In subsequent research, Shu, Payne and Sagara found that using the “live to” framing (with its undercurrent of longer life expectancy) could be an important nudge to encourage more people to delay when they begin to draw their Social Security retirement benefit.

Anyone eligible for Social Security can start collecting payments as early as age 62. But the payout is 25 percent to 30 percent less than if the recipient waits until full retirement age (somewhere between 66 and 67, depending on year of birth). Delaying until age 70 to start claiming delivers a benefit that is worth 76 percent more than the age-62 benefit. That’s a risk-free return no T-bond can deliver these days. From that economic lens it makes great sense to delay drawing Social Security early and either delay retirement altogether or tap other retirement income sources in the early going. Yet most recipients claim earlier, not later, forgoing the opportunity to generate the insurance of greater retirement income at a later age. The researchers found that when they presented the mortality issue as a “live to” proposition, individuals were more inclined to wait longer to start drawing their Social Security retirement benefit, and make other economically rational retirement decisions.

The authors also found that the behavioral tic of “loss aversion” is another contributing factor in our desire to claim earlier, a sense of losing out if we were to die sooner and not get out of Social Security what we put into it. Related to loss aversion, feelings of ownership about prospective Social Security payments (“That’s my money!”) prompt early benefit-taking.

So, rather than wait to optimize our eventual payout — the best hedge against longevity — we’re inclined to jump sooner.

But when confronted with greater longevity, we find the value of the higher later-life payout more compelling. “A longer predicted life expectancy predicts less myopic behavior, with individuals choosing to delay Social Security claiming, expressing a preference for life annuities, choosing equities, and saving a higher percentage of their income for retirement,” wrote Shu, Payne and Sagara.

Guaranteed Income? Yes! Annuity? Meh.

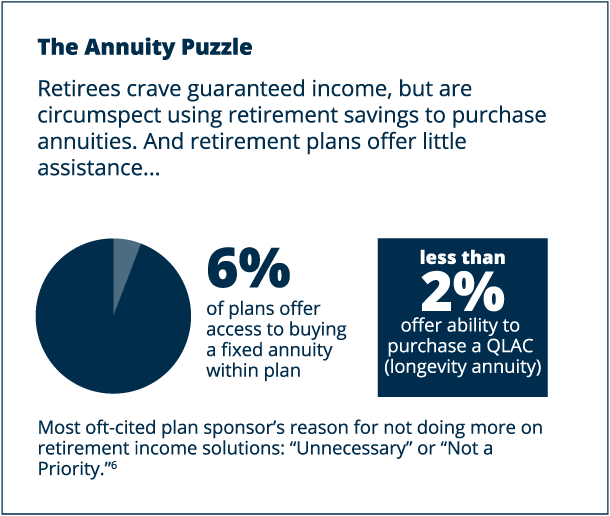

Another decumulation challenge is the prospect of letting go of some retirement assets to get something of value in return. That is, using retirement funds to purchase an annuity. It’s not exactly surprising that if you ask a room of retirees if they would like a guaranteed stream of income for life, just about every hand in the room will raise. But then suggest taking a portion of their 401(k) or other retirement assets to buy a fixed annuity — that is, fund a pension for life — and the room goes cold.

This so-called “annuity puzzle” has attracted and confounded researchers for decades. Franco Modigliani name-checked it in his 1985 Nobel Prize acceptance speech.

More recently, Benartzi and Thaler, along with Alessandro Previtero of the University of Western Ontario, found that there is not an inherent dislike of annuities, given that retirees aren’t prone to thumb their noses at Social Security or a traditional pension, which are de facto annuities. But when staring at large 401(k) and IRA balances, the notion of spending a portion to buy guaranteed income via a fixed annuity just grates at our human nature. “The purchaser has to write a big check to get a series of small checks, which may simply look like a bad deal to a naïve consumer. It is well established that once people think they have something, they become reluctant to give it up,” they wrote in The Journal of Economic Perspectives. “An annuity should be viewed as a risk-reducing strategy, but it is instead often considered a gamble.” Moreover, currently, very few 401(k) plans offer a seamless way for savers to purchase basic fixed annuities within a plan. Plans have also been slow to offer longevity annuities, despite the U.S. Treasury Department’s green-lighting them within defined contribution plans in 2014.

Shu, Payne and Zeithammer found that tweaking the marketing message of annuities could boost demand without having to add a penny more to the payout of the investment. In their research for “Consumer Preferences for Annuities: Beyond NPV” the authors found that the prospect of investing in a financially secure insurer offering policy features such as an inflation adjustment or a guaranteed payout for a set number of years (to the annuitant or a beneficiary) can nudge consumer preference. Shu, Zeithammer and Payne also discovered that how those factors are displayed in marketing literature impacts demand. Those insights deliver a marketing opportunity to insurers — and to sponsors of 401(k) and 403(b) plans — looking to encourage consumers to consider the value of annuitizing a portion of their retirement savings.

To the extent that government regulators bear down on creating automated nudges for the decumulation, this research could help craft compelling messaging for retirees.

A focus on information architecture — how our choices are presented and framed — is also at the heart of new research from Benartzi, UCLA Anderson’s Hershfield and Daniel Goldstein, principal researcher at Microsoft Research. They set out to determine what engenders the better retirement saving behavior: showing the lump sum value of a retirement account worth $1 million, or the actuarially equivalent $5,000 monthly income that can be generated by that lump sum. The $1 million frame appeals to retirees who have an “illusion of wealth.” A preference for the monthly payout frame is a function of an “illusion of poverty.”

The research suggests retirement plan sponsors and brokerages that are the keepers of the $15 trillion sitting in defined-contribution and IRA plans would do investors a solid if they accentuated the annuity value, not the net worth lump sum. Goldstein, Hershfield and Benartzi wrote: “We speculate that perceptions of wealth as an annuity are more likely to lead to satisfactory choices because it is easier to estimate a month’s expenses than to estimate expenses over all of retirement.” Yet log in to your retirement account and the big-font display likely touts only your total assets. A 2013 proposal from the U.S. Department of Labor that would require retirement plan statements to include an estimate of retirement income, not just current assets, has yet to get green lighted. And just 2 percent of plan sponsors surveyed by benefits consultant Aon Hewitt designated “encouraging lifetime income” as a clear priority to address. “To help people reason better about spending in retirement, retirement plan providers should provide people with their projected monthly income at retirement based on their current saving behavior instead of the current practice of providing only account balances,” wrote the authors.

Providing that frame doesn’t increase plan costs, and it offers the big-ticket payoff of helping the next wave of retirees become successful decumulators.

Featured Faculty

-

Shlomo Benartzi

Professor of Behavioral Decision Making

-

Suzanne Shu

Professor Emeritus of Marketing

-

Robert Zeithammer

Professor of Marketing

About the Research

Benartzi, S., Previtero A., & Thaler, R. (2011). Annuitization puzzles. Journal of Economic Perspectives, 25(4), 143-164. doi: 10.1257/jep.25.4.143

Payne, J.W., Sagara, N., Shu S.B., Appelt, K.C., & Johnson, E.J. (2013). Life expectancy as a constructed belief: Evidence of a live-to or die-by framing effect. Journal of Risk and Uncertainty, 46(1), 27-50. doi: 10.1007/s11166-012-9158-0

Shu, S.B., Payne, J.W., & Sagara, N. (2014, August). The psychology of SSA claiming decisions: Toward the understanding and design of interventions. Paper presented at the meeting of the Retirement Research Consortium, Washington, D.C.

Shu, S.B., Zeithammer, R., & Payne, J.W. (2013). Consumer Preferences for Annuities: Beyond NPV.

Thaler, R.H. & Benartzi, S. (2004). Save More Tomorrow™: Using behavioral economics to increase employee saving. Journal of Political Economy, 112(S1), pt. 2, S164–S187. doi: 10.1086/380085

Footnotes (Infographics)

1 Plan Sponsor Council of America 2016 survey of profit sharing and 401(k) plans, Table 90.

2 PSCA 2017 survey, Table 96.

3 JP Morgan 2017 Defined Contribution Plan Sponsor Survey Findings.

4 Morningstar 2017 Target-Date Fund Landscape.

5 Vanguard: How America Saves 2017, Figure 66.

6 Callan Associates 2017 Defined Contribution Trends Survey.

7 Alicia H. Munnell and Anqi Chen (2015), Center for Retirement Research, Boston College, “Trends in Social Security Claiming.”