A unique data set provides fresh insights for the growing institutional investor market

More than one third of households that rent live in a single-family home rather than an apartment building. While still dominated by mom-and-pop landlords, single-family rentals — valued at an estimated $2.3 trillion — are increasingly getting the attention of the institutional investor class.

Invitation Homes (INVH), the public face of Blackstone private equity’s play in single-family rentals, has a current market capitalization near $12 billion. In the past year, Fannie Mae and Freddie Mac have begun to dip their toes into guaranteeing single-family rental bonds.

With homeownership rates dropping amid an affordability squeeze and stricter mortgage qualifying standards, the rental market is expected to play an increasingly larger role in American’s housing picture (approximately 35 percent of households now rent). Yet there is a dearth of comprehensive return analysis of single-family rentals for investors to turn to. A quirk of existing research has been to focus either on the net yield or the price-appreciation potential, each to the exclusion of the other. (Net yield is calculated by subtracting expenses from gross rental income and dividing that by the purchase price of the property.)

Opt In to the Review Monthly Email Update.

“Each component contributes approximately equally to the aggregate U.S. portfolio of housing returns, so excluding one component excludes half of total returns on average,” write Andrew Demers, a real estate specialist at Structured Portfolio Management, and UCLA Anderson’s Andrea Eisfeldt, in a working paper.

Demers and Eisfeldt provide a total-picture analysis by studying net yield and price appreciation of single-family rental homes, in tandem, in the 30 largest metro areas between 1986 and 2014.

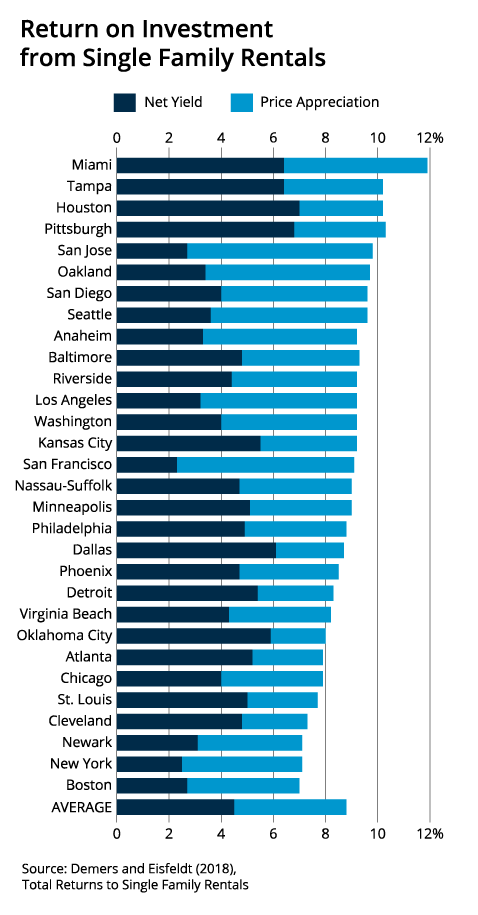

The average 4.5 percent net yield may seem like a bond-like meh; but add in the 4.3 percent average return from price appreciation and the near 9 percent average total return for single-family homes gives the 10 percent plus long-term annualized return of the S&P 500 a run for its money.

The nearly three decades of data suggest that the investment opportunity in single-family rentals is not a one-time event tied to the foreclosure boom (investors scooped up homes on the cheap) during the housing crisis that began in 2008. The crisis was, of course, a one-time buying opportunity in terms of low home prices and, owing to widespread foreclosures, a chance to sidestep the hefty roughly 5 percent real estate agent transaction fee, Eisfeldt said in a conversation about the paper. (Can you imagine Wall Street investment funds paying a 5 percent fee to buy a bond?)

The authors discovered a wide divergence in the underlying components of total return for single-family homes. Net yields are the major driver of total return in cities where home prices are lower, and price appreciation is the bigger factor in markets where home prices are higher. Overall, the cheaper homes delivering higher net yields had the best average total returns.

Among the lowest-priced quintile of homes in their study, the average 9.36 percent total return is the sum of a 6.1 percent net yield and 3.24 percentage points in price appreciation. In the highest-priced quintile of homes, the 8.3 percent total return is the sum of 2.92 percent of yield and 5.34 percentage points of price appreciation.

If you are an investor most interested in current income, you might want to focus on a market with high net yields. For instance, Houston’s annualized 10.2 percent total return is derived from a 7 percent net yield and barely 3 percentage points of price appreciation.

If you’re a Blackstone type looking to optimize your eventual cash-out price, you might be more interested in markets where price appreciation is the main driver. San Francisco’s 9.1 percent total return was mostly the result of an annualized average 6.8 percent price rise.

And if you’re a public policymaker, understanding the total return big picture can provide more confidence in backing projects.

The authors also provide push-back on the notion that in-demand coastal areas are the best investments. While those markets indeed have the highest prices, the higher net yields in flyover cities helped generate better total returns.

Pittsburgh and Houston each had average 10.2% total returns, with more than two thirds of it coming from net yield. Kansas City and Minneapolis had total returns above the national average. Boston and New York’s total returns were below the 30-city average.

Moreover, Demers and Eisfeldt find that net rental yields tend to be less volatile than price appreciation, thus less expensive markets that derive more of their total return from net yields provide a smoother ride for investors.

Featured Faculty

-

Andrea L. Eisfeldt

Laurence D. and Lori W. Fink Endowed Chair in Finance and Professor of Finance

About the Research

Demers, A., & Eisfeldt, A. (2018). Total returns to single family rentals.